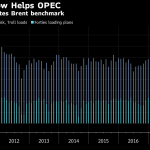

Ineos may have just put solid resistance in oil prices. The pipeline operator said yesterday it is expected to complete repairs at the end of this month on the Forties pipeline in the North Sea. It will begin a gradual restart to the 450,000 barrel per day crude oil pipeline and return it to normal […]

Read MoreWill the Restart of the Forties Return Bears After the Holiday?