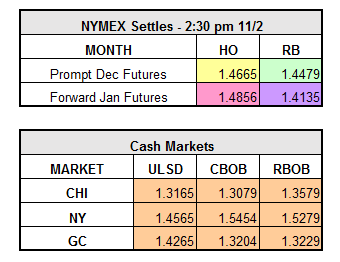

Last night the Chicago Cubs finally ended their 100+ year championship drought, and now we can all focus our attention on trying to get a better idea of what this market is going to do heading into 2017. The market was supported early this morning by a weaker U.S. dollar, but the prolonged rumors being spread around about a dubious OPEC agreement at the end of the month are putting pressure back on the market and keeping it somewhat stagnant across the board. As of 11:30 a.m. ET, distillates are down $0.0075, gasoline is up $0.0110 and crude is down $0.40.

Also adding strength to the market this morning was another Nigerian militant attack on the country’s oil infrastructure, raising concerns about a supply interruption.

As the day has moved along, crude and refined products have reversed course, reflecting the massive build in crude inventory indicated by this week’s API and DOE reports.

Switching over to the news that shook the market earlier this week, Line 1 of the Colonial Pipeline is still closed. However, Colonial pipeline reported that there is a tentative start time for Line 1 to resume operations on Saturday around noon ET. The key word in that sentence is “tentative.” Don’t be so sure that everything is going to be back to normal in short order. A devastating event like this can have repercussions that move downstream and affect supply for days, weeks, sometimes months. Keep an eye on this blog to stay up to date on Colonial pipeline news!

Interesting news:

- Remember Brexit? U.K. High Court rules Brexit cannot take place without parliamentary approval.

- The Saudis raise their December crude loadings to European and Asian buyers.

- CNBC reports that “OPEC’s game of ‘Deal or No Deal” could push oil prices back below $30 a barrel.