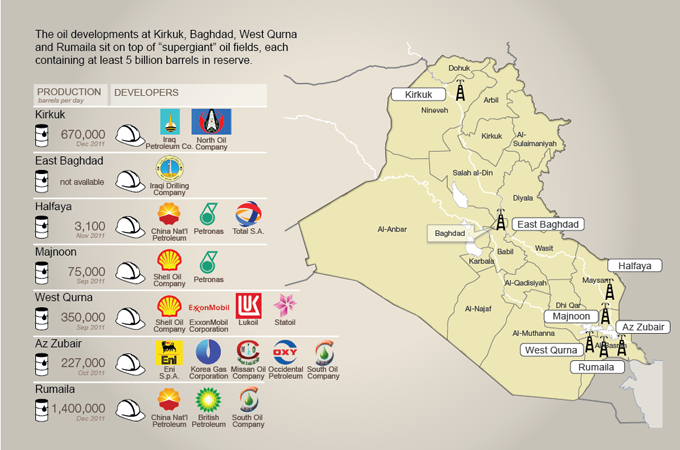

On September 25th the Kurdish Regional Government (KRG) voted for their independence and ever since there has been uncertainty in the region. The stability of the Middle East is called into question yet again to start the trading week. Tensions were escalating quickly in the city of Kirkuk as Iraqi forces entered the city and solidified control over the oil rich fields of Bai Hassan and Avana. Reuters reported that the oil fields were briefly shut down Monday morning due to “security concerns.” These oil fields are responsible for roughly 350,000 barrels a day of production. Based on the bullish move in the markets this morning, it is safe to say this flare-up in tensions is playing a major role in the energy sector. After Iraqi forces were able to control the northern region of the country’s oil fields, the KRG government was reported as saying that the regions’ oil was still flowing and that they would not attempt to halt it in any way.

The reason for such a large market move up today was not only due to the temporary shutdown of those two oil fields but the instability of that region which is responsible for nearly 600,000 BPD in production. To make matters worse for the KRG, Turkey has also agreed to shut off a pipeline that is directly controlled by the KRG government if Baghdad requests them to do so. In addition, we must also acknowledge potential continued instability to the region with the possibility of President Trump terminating the Iran deal. This is a heavy topic of discussion given there are now talks of possible new sanctions against Iran that would inhibit them from moving forward with their nuclear program. These sanctions could come in ways of limiting their oil exports, which is a large portion of the countries’ life blood, and financial stability. The German Foreign Minister was cited as saying “As Europeans together, we are very worried that the decision of the U.S. President could lead us back into military confrontation with Iran.” A less stable Iran, and further instability in the Middle East, again, is a direct foundation to the bullish market movement today.

The Saudi’s haven’t necessarily been quiet during all of this and have used their “oil kingpin” status to do what they can to raise the price per barrel as well. Given their status within OPEC, and the weight they throw around in the oil market, they came forth and opened up about how they will conduct the “deepest customer allocation cuts in its history” according to Reuters. The cuts will consist of roughly 560,000 barrels per day next month. The Saudi’s, time and time again, tend to put out this kind of news as often as they can in order to help boost the rebalancing effort that OPEC has in place currently.

Lastly, in the U.S. you are seeing more factors that have contributed to the oil market rally as of late. To begin with, one of the easier price moving indicators, inventories, have been declining due to the devastating hurricanes that ripped through the U.S. and its territories. The draws in our U.S. crude stockpiles have helped boost the market temporarily but those gains are short lived because of the current record breaking exports. These exports seem to be fueled by the increased volumes sent to China. The U.S. currently has 11 tankers arriving in China by November, filled with nearly all U.S. product and another dozen right behind them scheduled to arrive between the end of the year and January 2018. The Energy Information Administration (EIA) is reported as saying that exports of U.S. crude have hit a record of 1.98 million barrels per day in September. With China, India, and others looking to diversify the product they are importing, the price spreads will benefit the U.S. as exports appear to continue their trend higher.