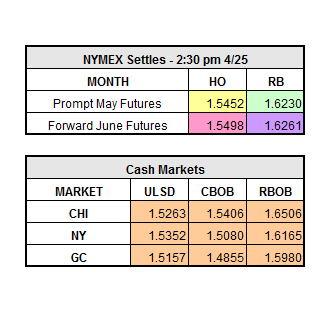

Yesterday the market was off all day and then had a small rally at close. June WTI closed up $0.33 to $49.56/bbl, May HO closed up $0.0025 to $1.5452/gal, and May RBOB finished up $0.0016 to $1.6230/gal. The market was off last night and continues to trade down this morning due to the bearish API statistics released last night. The API stats showed a build in crude inventories of 897,000 barrels, a surprising statistic because expectations were a 1.7 million barrel draw. The gasoline build of 4.4 million barrels was an even bigger surprise, since a 1 million barrel draw was expected. Distillates drew 36,000 barrels, which was a bit smaller than what was expected.

The DOE statistics released at 10:30 a.m. ET differed slightly from the APIs. The DOEs showed a draw of 3.6 million barrels in crude inventories. The decline is mostly made up of a 1.2 million draw from Cushing, 1.9 million barrel draw from PADD II and a 1.2 million barrel draw in PADD III. Refined products both showed a substantial build. Distillate inventories built 2.7 million barrels and gasoline inventories built 3.4 million barrels. The market reacted as soon as the stats were released and initially oil prices started to come back some, probably driven by the reported draw in crude. As of 11:10 a.m. ET, WTI is now trading positive $0.23/bbl, HO is down about $0.01/gal, and RBOB is still down $0.0250/gal.

The concern is that the supply glut continues even after the OPEC output cuts since the beginning of the year. The next piece of news is whether or not OPEC agrees to continue cuts into the second half of the year. The downward trend continues for refined products; market closes below the following support levels could mean even further weakness: WTI 48.91, HO 1.5336, and RBOB 1.6007.